Understanding Bankruptcy Options

- 1 - What is Bankruptcy?

- 2 - Types of Bankruptcy

- 3 - How to Choose the Right Bankruptcy Option

- 4 - Common Myths About Bankruptcy

- 5 - How Bankruptcy Affects Your Financial Future

1 - What is Bankruptcy?

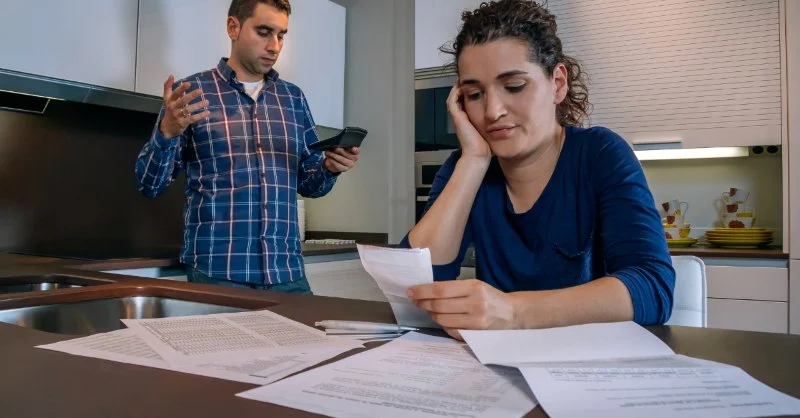

Bankruptcy is a legal process that provides individuals or businesses facing overwhelming debt with an opportunity to eliminate or repay their financial obligations under the protection of the court. While it can be a difficult decision, it can also offer a fresh financial start for those who qualify. Understanding the various bankruptcy options available can help individuals make an informed decision about their financial future.

In the United States, bankruptcy law is governed by federal law, and the process is handled through the bankruptcy courts. Filing for bankruptcy can help protect assets, stop creditor harassment, and provide relief from debt that seems impossible to overcome.

Law Office of Scott Pactor

Beverly HillsLos Angeles CountyCalifornia

9150 Wilshire Blvd, Beverly Hills, CA 90212, USA

2 - Types of Bankruptcy

There are several types of bankruptcy filings, each with different eligibility requirements, processes, and outcomes. The most common types of bankruptcy are Chapter 7, Chapter 11, and Chapter 13. Here's a closer look at each:

1. Chapter 7 Bankruptcy: Also known as "liquidation bankruptcy," Chapter 7 is typically the quickest and simplest option. It allows for the discharge of most unsecured debts, such as credit card balances and medical bills. However, it may require the liquidation of some assets to pay creditors. Individuals with a steady income may not qualify for Chapter 7, as it is typically reserved for those with lower incomes and few assets.

2. Chapter 13 Bankruptcy: Chapter 13 is a reorganization bankruptcy option that allows individuals with a steady income to create a repayment plan for their debts over three to five years. This option is often chosen by people who want to keep their property, such as a home, and work out a manageable payment plan with creditors. At the end of the repayment period, any remaining eligible debts may be discharged.

3. Chapter 11 Bankruptcy: Chapter 11 bankruptcy is typically used by businesses, though individuals with significant debts may also file for Chapter 11. This type of bankruptcy allows the debtor to restructure their debts and continue operating while making payments according to a court-approved plan. It is a more complex and expensive process compared to Chapter 7 or Chapter 13, and is generally used for larger businesses or individuals with substantial assets and debts.

J. Witherspoon Legal & Mediation Services

32 N West St Ste 100, Waukegan, IL 60085, USA

3 - How to Choose the Right Bankruptcy Option

Choosing the right bankruptcy option depends on several factors, including your income, assets, the types of debts you owe, and your long-term financial goals. Here are some factors to consider when deciding which bankruptcy option is right for you:

1. Your Income: If you have a steady income but struggle with significant unsecured debts, Chapter 13 may be a better option, as it allows you to create a manageable repayment plan. If you don’t have the income to repay debts, Chapter 7 may be the more appropriate choice, as it discharges most unsecured debts.

2. Your Assets: If you own significant assets, such as a home or business, and want to keep them, Chapter 13 might be your best bet, as it allows you to restructure debt without losing property. Chapter 7, on the other hand, could require you to liquidate non-exempt assets to pay creditors.

3. The Type of Debt: Some debts, like student loans, child support, and taxes, are not typically dischargeable through bankruptcy. If most of your debt falls into these categories, you may need to explore other options, such as debt settlement or negotiation.

4 - Common Myths About Bankruptcy

There are many misconceptions about bankruptcy that can prevent individuals from exploring this option when it might be beneficial. Here are some common myths:

1. Bankruptcy Will Ruin My Credit Forever: While bankruptcy can have a negative impact on your credit score, it doesn’t mean that you will never be able to rebuild your credit. In many cases, individuals who file for bankruptcy can start rebuilding their credit immediately after the process is complete by managing their finances responsibly.

2. I Will Lose All My Property: Many people believe that filing for bankruptcy will result in losing their home, car, or other personal property. However, this is not always the case. Exemptions exist that may allow you to keep certain assets, and Chapter 13 can help you keep your property while you repay your debts.

3. Bankruptcy Is Only for People Who Are Irresponsible: Bankruptcy is often misunderstood as a result of poor financial decisions. In reality, many people file for bankruptcy due to unexpected events such as medical emergencies, job loss, or divorce. Bankruptcy provides a legal way to deal with overwhelming debt, no matter how it occurred.

5 - How Bankruptcy Affects Your Financial Future

While bankruptcy can provide relief from overwhelming debt, it does come with long-term effects that should be carefully considered:

1. Impact on Credit Score: A bankruptcy filing will appear on your credit report and can significantly lower your credit score. However, over time, you can rebuild your credit by paying bills on time, keeping credit card balances low, and using secured credit cards or small loans.

2. Difficulty Securing Loans: After filing for bankruptcy, it may be more challenging to qualify for loans, especially for larger purchases like a home or car. However, some lenders specialize in working with individuals who have filed for bankruptcy, so it is still possible to obtain credit.

3. Financial Fresh Start: Despite the initial setbacks, bankruptcy offers a fresh start. It provides an opportunity to rebuild your finances, avoid creditor harassment, and make smarter financial decisions moving forward.

For more guidance on understanding bankruptcy options and how to make the best choice for your situation, visit Barber Law Hub for expert advice and resources.

Kuranty John2.0 (5 reviews)

Kuranty John2.0 (5 reviews) Scott H. Thomas0.0 (0 reviews)

Scott H. Thomas0.0 (0 reviews) H Taufiq Choudhury PC0.0 (0 reviews)

H Taufiq Choudhury PC0.0 (0 reviews) Kraut Law Group Criminal & DUI Lawyers5.0 (21 reviews)

Kraut Law Group Criminal & DUI Lawyers5.0 (21 reviews) Randy Fisher Law5.0 (4 reviews)

Randy Fisher Law5.0 (4 reviews) Formica Law Group | Injury & Accident Lawyers5.0 (15 reviews)

Formica Law Group | Injury & Accident Lawyers5.0 (15 reviews) How to Avoid Common Legal Mistakes When Buying a Home – Expert Advice

How to Avoid Common Legal Mistakes When Buying a Home – Expert Advice Law Made Simple: Understanding Child Custody Laws in Simple Terms

Law Made Simple: Understanding Child Custody Laws in Simple Terms How to Expunge a Criminal Record – A Complete Guide

How to Expunge a Criminal Record – A Complete Guide How to Choose the Right Lawyer for Your Case – Expert Legal Advice

How to Choose the Right Lawyer for Your Case – Expert Legal Advice Your Rights During a Police Stop – Expert Legal Advice for Citizens

Your Rights During a Police Stop – Expert Legal Advice for Citizens A Step-by-Step Guide to Writing a Will – Expert Legal Advice

A Step-by-Step Guide to Writing a Will – Expert Legal Advice